The Earth is getting hotter. Since 1890, science shows. Earth has warmed by 1.2 degrees Celsius (or 2.2 degrees Fahrenheit). That’s thanks to the carbon dioxide humans produce when they burn fossil fuels for heat and electricity.

If we don’t drop our carbon dioxide emissions, our climate could eventually be 4 degrees Celsius warmer than pre-industrial times. And while that’s an annual average, the actual temperature will have peaks and valleys. For example, in a 2010 Russian heat wave tied to climate change, temperatures hit 10 degrees Celsius higher than seasonal norms. That single heat wave killed tens of thousands of people.

This article describes the huge risks climate change poses for business – and how business can use adaptation to become more resilient to those shocks.

What Is Climate Risk? – Meaning and Examples

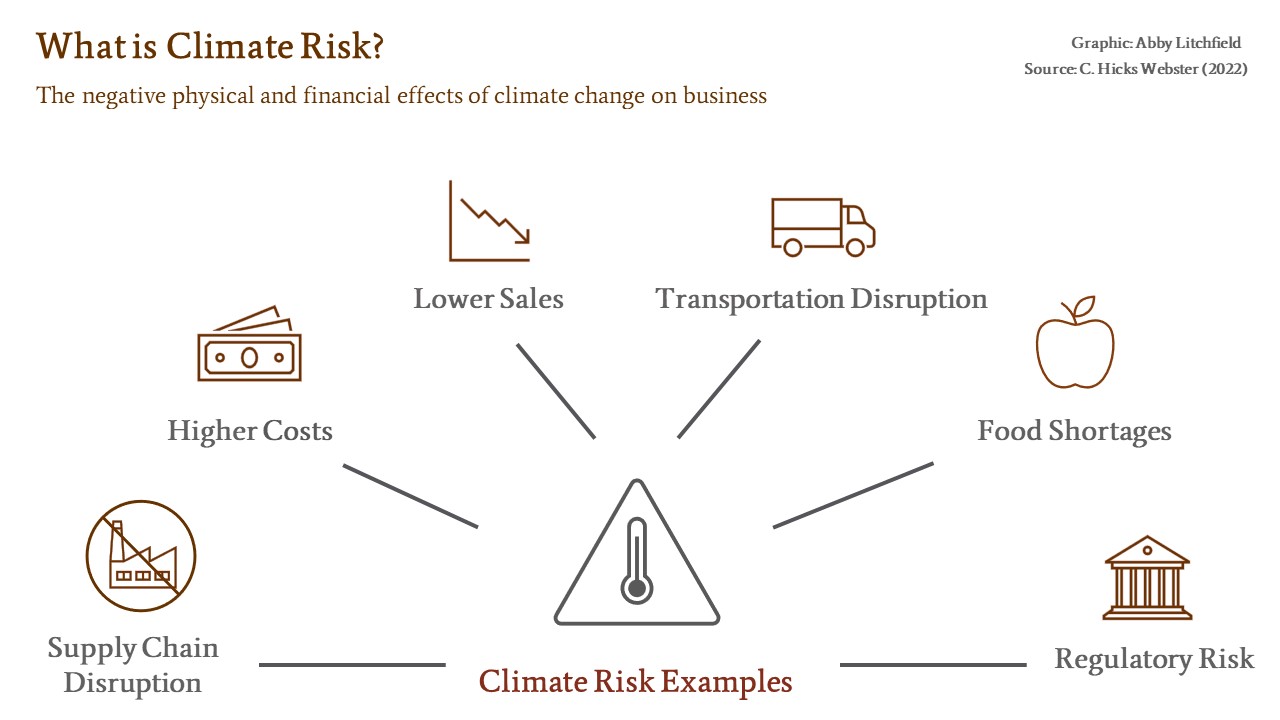

Climate risk refers to the negative physical and financial effects that global warming has for businesses.

Climate risk isn’t a ‘later’ issue. It’s a ‘now’ issue. Climate change is already increasing costs, lowering sales and disrupting operations globally. Here are some key areas of risk:

- Supply chain disruption: In 2021, a climate change-related typhoon in Malaysia caused local manufacturing to grind to a halt. Because Malaysia packages most of the semiconductors imported by the United States, the typhoon caused a semiconductor shortage that stopped operations for some US automakers.

- Higher costs: In 2019-20, Australia’s climate change-related bushfires burned more than 46 million acres of land and cost insurance companies USD 1.3 billion in claim payouts.

- Lower sales: Ski companies depend on long winters for sustainable revenue. The warming climate is leading to shorter, warmer winters, which in turn reduces the amount of revenue these seasonal businesses can generate.

- Transportation disruption: The Rhine River is one of Europe’s most important transportation channels. In recent years, droughts have led to record low water levels, which have stopped steel companies from shipping product and stopped tourism companies from running river cruises.

- Food shortages: Farmers rely on consistent water for crops. This summer, Italy experienced a warm, dry winter. In the spring, the local rivers did not receive their normal influx of melt water and many rivers dried up by early summer. This is expected to reduce Italy’s rice production by 30%. Pakistan and other countries have seen even worse impacts.

- Regulatory risk: As these negative impacts continue to grow, public pressure is mounting and governments are beginning to act. For example, in 2022, the U.S. Securities and Exchange Commission announced plans to require all publicly traded companies to report their emissions and climate-related risks. Companies not currently participating in voluntary carbon reporting will soon be scrambling to catch up.

The type and the amount of climate risk that companies face varies considerably by sector and location.

For example, Toronto, Canada will experience fewer intense storms related to global warming than will New Orleans, United States which is already vulnerable to hurricanes. That means that a building insurance company in New Orleans faces considerably greater climate risk than a building insurance company in Toronto.

However, that doesn’t mean all companies in Ontario face low climate risks. Ontario is known for its agriculture, and agriculture is particularly vulnerable to changing weather patterns. Droughts or floods can destroy crops and put Ontario-based farmers at significant risk.

What Is Climate Change Adaptation?

So, what can you do to protect your business from climate risk? You can boost your resilience through adaptation. Here’s what climate change adaptation and resilience mean:

Resilience is a state of being. It’s when a system has the capacity to absorb a shock, like severe weather events from climate change. For example, what would happen if drought conditions caused a shipping channel to dry up, and one of your suppliers couldn’t ship for 3 weeks?

Would your own operations grind to a halt because you were missing a key input? If so, your business lacks resilience to climate change. Or, would you be able to keep going? Perhaps you have surplus supply storage, or another supplier who sells the same product. In this case, your business would be resilient.

Adaptation, on the other hand, is an action. It’s when a system – like your business – changes its structure or activities to become more resilient to shocks. For example, if you knew that climate change could interrupt your supply chain, you could start holding extra inventory. That action would be adaptation.

In other words, climate change adaptation is something you do, to become more resilient to severe weather from climate change.

Examples of Business Adaptation to Climate Change

Mountain Equipment Company (MEC) is an outdoor gear company. They sell everything from raincoats to parkas, and from bikes to skis.

MEC bakes climate change adaption right into their core business processes. Leaders routinely consider climate risks, alongside all other types of risk, in their strategic planning and investment activities.

MEC identified uncertainty in weather patterns as a major risk. They had no way of knowing how the weather would behave, yet weather had huge power over their company. For example:

- If seasons become shorter or longer, that changes the demand for seasonal products.

- Extreme weather events could impact their whole supply chain, from increasing the price of raw materials, to interrupting shipping, to flooding stores and distribution centres.

MEC is doing two things to adapt proactively to that risk.

- Reduce uncertainty. MEC’s accountants are collecting data from the local weather service and comparing that to their sales data to understand exactly how weather changes impact sales. This information will help them make more informed decisions about their future.

- Strengthen sourcing. They’ve diversified sourcing, finding more than one supplier for the same product or material. If flooding or drought wipes out an area’s cotton supply, they can access other sourcing options. Alternatively, they could help suppliers become more resilient, or draw on more local sources.

4 Reasons Businesses Should Adapt to Climate Change

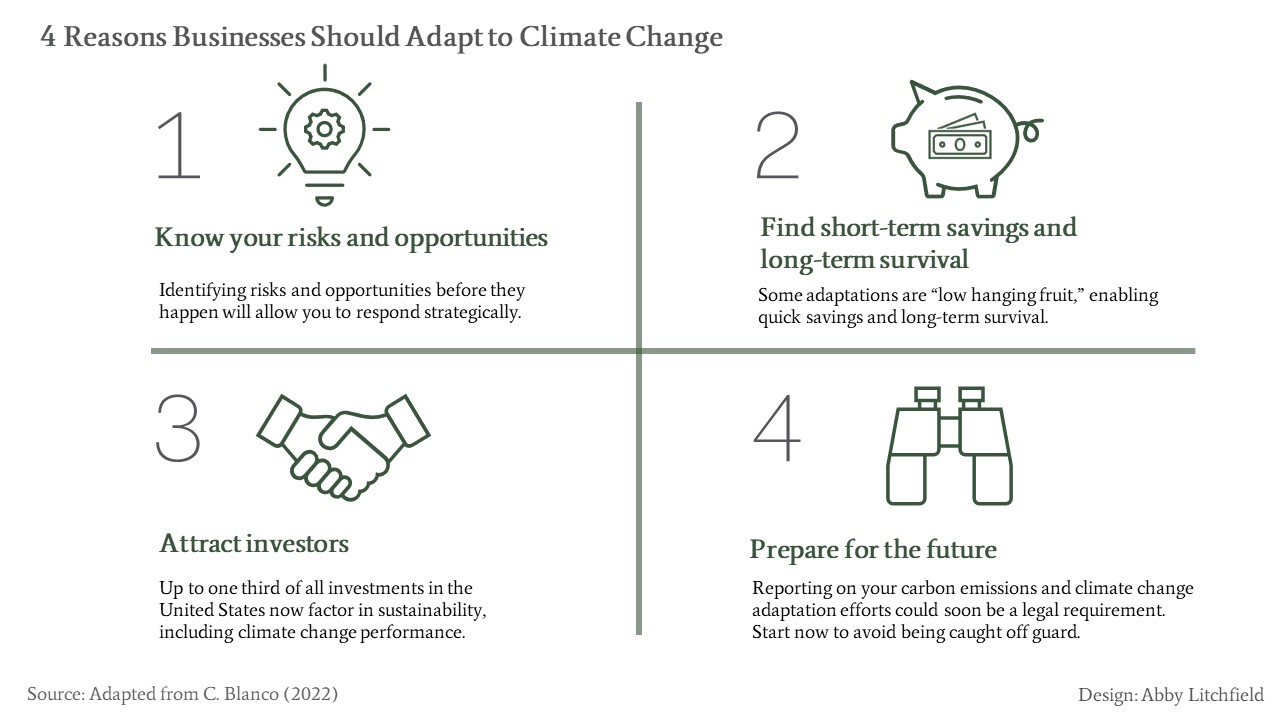

Climate change adaptation has four key benefits for businesses:

1. Know your risks and opportunities: If you aren’t intentionally looking for risks and opportunities, they will likely remain invisible.

For example, in 2007 Walmart began reporting on its climate performance to an organization called CDP. CDP requires reporting companies to identify their climate-related risk and opportunities.

At the time, Walmart thought its risks were relatively low – but they were wrong.

Climate change brought Walmart many risks – and opportunities. Risks include:

- Higher cooling and refrigeration costs because of higher outside temperatures.

- Increased financial burden from carbon taxes.

- Higher supply costs because of global food shortages and transportation holdups.

On the bright side, they can generate new sales from innovative low-carbon products.

Conducting their risk assessment made them readier for whatever the future brings.

2. Find short-term savings and survival: Businesses can often find ways to adapt that bring short-term financial payback and enable future stability and survival. For example, Suncor is reducing its water withdrawal from the Athabasca River through more efficient operations. That means lower input costs now and less risk of water shortages as the Athabasca’s water supply becomes less stable.

3. Attract investors: Investors increasingly want to know that the companies they buy into are adapting to climate change. These investors know that climate change will impact companies’ bottom lines, and therefore shareholder earnings. Up to one third of all investments in the United States now factor in sustainability, including climate change performance.

4. Prepare for the future: Soon climate change adaptation may be non-negotiable. Both the United States and the European Union are making climate reporting a ‘must’ for publicly traded companies. If you identify and adapt to your risks and opportunities now, you won’t be caught off guard when it becomes mandatory.

10 Tips for Corporate Climate Change Adaptation

As your company plans its approach to climate change risks and opportunities, keep the following tips in mind!

1. Don’t wait. The climate is changing, and the world’s response is shifting quickly. Don’t be caught off guard. Start understanding – and adapting to – the reality of climate change

2. Build adaption into existing business processes. Don’t let your climate response be a sideline. Bake climate risk into your core strategic planning processes, including having senior executives in charge.

3. Think bigger (longer timeline, more stakeholders). Climate change is a long-term challenge – it’s not going away in this lifetime. And climate change impacts everyone.

To address the long-term timeline, go beyond quarterly or annual planning. How will your business need to be different in 5 years? 10 years? 20 years?

You’ll also need to think about a range of stakeholders. How will climate change (or your company’s proposed adaptation activities) affect your employees, suppliers, customers, and local communities and ecosystems? Understanding these connections is called ‘systems thinking’ and it leads to better decisions.

4. Involve employees: Your front-line employees may see risks that you can’t see and have solutions you may not have thought of. Plus, involving them in your planning process will reduce resistance to changes.

Lyn Brown, Vice President of Marketing and Communications at Alberta Innovates, works on climate change adaptation in Alberta’s energy sector. Her recommendations? “Let employees know that they have a place in the future, that they have valuable ideas to shape it… In my experience, resistance to change often comes from a place of fear. So, invite different perspectives…Do this early and often.”

5. Support those disadvantaged by changes: Your company’s response to climate change will affect your stakeholders differently. Be aware of those who will be hurt by your actions and seek to ease their transition. For example, when coal-fired power plants close, companies and government can help workers by providing transition support directly or through non-profit organizations.

6. Collaborate outside your firm. Climate change is going to impact you and your competitors in similar ways – so why not work together on solutions? A great example of this is ClimateWise. Through this organization, 40 global insurance companies work together to analyze and reduce their climate-related risks.

7. Learn from the leaders. There’s no need to reinvent the wheel. Find out what others in your and others’ sectors are doing and let their ideas inspire you! (NBS has some great case studies from the travel, transportation, and utilities)

8. Expect uncertainty and explore multiple options: Even a robust risk assessment can’t provide certainty about the future. Build “if-then” scenarios. For example, invest in more than one technology, so that you’re ready regardless of which technology gains public traction. General Electric, for example, expanded beyond gas and steam turbine into producing wind turbines.

9. Include mitigation (emissions reduction) in your adaptation strategy: Mitigation will reduce the speed and overall intensity of climate change, which reduces the need for rapid adaptation. Therefore, it’s a critical part of any adaptation strategy.

10. Report on your adaptation efforts: Many organizations, such as CDP or Sustainalytics, compile climate change information from companies and share the data with investors and stakeholders. (Ideally, this reporting should be ‘double materiality’ – meaning it describes how climate change will impact the company, and also how the company impacts communities and the environment.) These reporting frameworks can give your efforts more structure and legitimacy. Plus, voluntary reporting now will help you prepare for a future where reporting isn’t an option.

Additional Resources

- NBS Primer on Climate Change

- Managing the Business Risks and Opportunities of Climate Change

- Weathering the Storm: Four Steps to Prepare Your Company for Climate Change

- How to Benefit from a Sustainability Transition

- 5 Ways Climate Change Adaptation Improves your Bottom Line

- How to Reduce Climate Costs Using Nature

- How to Make the Climate Transition Fair: Lessons from Australia

- How Workers Can Thrive in the Green Transition

- Carbon Reporting Can Help Your Business

- How an Innovative Insurance Product Helps Clients Weather Climate Change

- Developing a Data Driven Climate Strategy – A Case Study

About the Series

“The Basics” provides essential knowledge about core business sustainability topics. All articles are written or reviewed by an expert in the field. The Network for Business Sustainability builds these articles for business leaders thinking ahead.

About the Authors

Chelsea Hicks-Webster spent her master’s degree studying ecosystem health in Kenya and is the former Operations Manager for The Network for Business Sustainability. She’s also a certified life coach. Chelsea now splits her time between her two passion projects; sustainability writing and editing, and helping over-stressed mothers improve their mental health and find more joy in life.

Review of this article was provided by Dr. Jury Gualandris, director of the Network for Business Sustainability and associate professor of Operations Management and Sustainability.

Add a Comment

This site uses User Verification plugin to reduce spam. See how your comment data is processed.This site uses User Verification plugin to reduce spam. See how your comment data is processed.